What salary should I pay myself as a director?

The new tax year is here! Now is the perfect time to consider the most tax-efficient remuneration structure for 2022/23 with payroll. There are some things that have changed from 2021/22, these are highlighted below:

What has changed

- Employees national insurance threshold increased to £12,570 (£1047.50 per month), from July 2022.

- Employees’ national insurance has increased by 1.25% to 13.25% (3.25% on income above (£50,270)

- Employers’ national insurance threshold rises to £9,100 per year (£758 per month)

- Employers National Insurance has increased by 1.25% to 15.05%

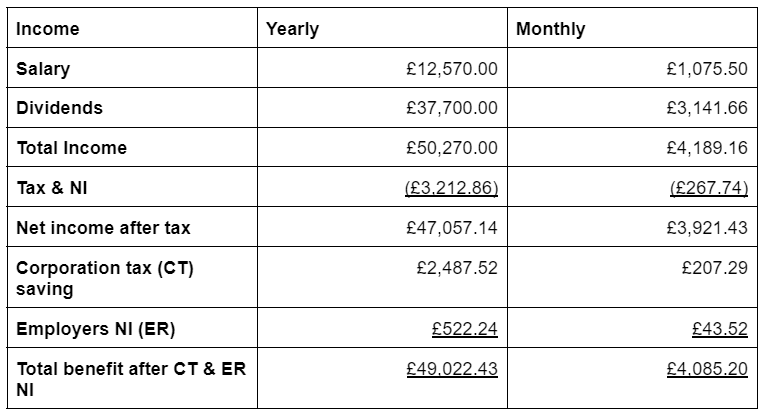

Therefore an annual salary package (including bonuses) of £12,570 will ensure that the director pays no employee NI. The saving in Corporation Tax will mean it is more efficient to pay a little bit of the employer’s national insurance.

Possible Issues

There are some key considerations that will affect the advice given, this will mean that discussing a bespoke remuneration structure would benefit you. These circumstances include (but are not limited to):

- You have other income declared through your self-assessment tax return

- You have a requirement to take remuneration in excess of the basic rate band

- Your company has net liabilities and cannot afford to declare dividends

Contact us to discuss the most beneficial structure for your specific circumstances.